Building Boldly, Failing Forward

This is the obituary of Asistensi, my ‘Capolavoro’ and the same for more than two hundred wonderful and talented persons who poured their hearts into the work of their lives.

In Asistensi we built the world’s first real solution to a massive problem for society: the lack of financial protection in healthcare expenses for migrants, specifically the lack of coverage for the families they support and stay at their home countries. Key accomplishments we can feel proud about this endeavour of include:

Building a membership base of over 40,000 persons across 55 countries.

Delivering over 35,000 health services across 6 countries and 14 time zones (from LATAM to Southeast Asia) with excellent customer service (4.3 Trustpilot score) and a 50% medical loss ratio.

Building the world’s first and only regulatory stack that enabled selling insurance cross-border. This included obtaining two health insurance carrier licenses, notably one of which was in the USA, and establishing risk sharing partnerships with the #1 ranked health insurance carriers in 7 countries.

Building an Multy Level Marketing - MLM affiliate program of more than 2,500 members in 115 cities with a lead to conversion ratio of 40%.

Raising more than USD 24 million in funding: USD 20 million from VCs and USD 4 million in debt. Albeit unfortunately these funds did not see a return on investment, these investors were real visionary supporters until the last minute and I will be forever grateful.

Building and leading a team of 260+ employees across 7 countries within a culture that was a growth platform for exceptional people.

The spoiler of this story? It worked but we failed while daring greatly.

It worked because:

Our first market to launch was cash flow positive and the remaining five had a path to do so with only c.10k policies. We had positive net contribution margin after acquisition costs in the 10 to 15 percent range after just three months of our launch and every month thereafter. Some markets had net margins as high as 30 percent.

We reached USD 8mm in ARR with customer acquisition costs that were below the actuarial limits’ consistently month after month after month, only spiking temporarily when we launched a new market. We had an efficient and scalable go-to-market channel which was our affiliate program (more on this below). These are the keystone acid tests of product market fit.

Our medical loss ratios stood at 50% and this was stable for all cohorts (vs. 85% for the industry).

Customers were delighted with the service. Not only because of the 4.3 Trustpilot score and 80% NPS which is 3x the insurance industry, but also because less than 1% of our 35,000+ medical services resulted in a customer service contact or complaint.

We failed because:

Fundraising winds changed when our sails were fully deployed towards market expansion (we launched one country every three months during 15 months) and we got caught in the market meltdown of VC funding with too much burn and not enough runway.

A Series B round with a strategic lead investor that gave us a USD 17mm binding term sheet fell apart after three months of closing work and left us with one month of cash in the bank. (why and learnings below).

We did too little too late to control customer churn in our second largest market (although elsewhere it was not a problem, for some investors it was a bad omen).

We invested too much of the development bandwidth for our tech platform into launching new markets and postponed too much creating efficient processes which in turn snowballed manual processes, headcount and ultimately burn.

A “build it and they will come” mentality towards margins in some markets (more on this below).

Having our HQ outside one of our key markets (also more on this below).

We launched and achieved scale in a market that was untouchable to many investors – Venezuela- despite this reflecting our execution capabilities in extremely difficult markets.

Also, to say it upfront and clearly: all insureds will continue to have the coverage they paid for and the insurance licenses will continue to remain solvent, if anything with reinforced financial support from new owners. The business in Venezuela will continue ever stronger albeit most likely under a different brand name, owners and without the international distribution capabilities. If you are a customer or affiliate and have questions about your coverage or referrals feel free to contact us directly at info@asistensi.com.

In the following sections I will also share information useful to those that want to address similar problems such as how to actually crack the problem of selling insurance cross-border legally, how to lower medical loss ratios while improving customer experience and how to build a positive culture in a fast growth startup. I will share a lot of information and materials, more than what is usually shared in startup obituaries, with the hope that someone picks up these pieces and uses them to build something great in the benefit of the millions of migrants that are trying to get ahead while taking care of their families back home.

This was the summary, if you are still interested in reading the extended version here goes the full story:

What was Asistensi about?

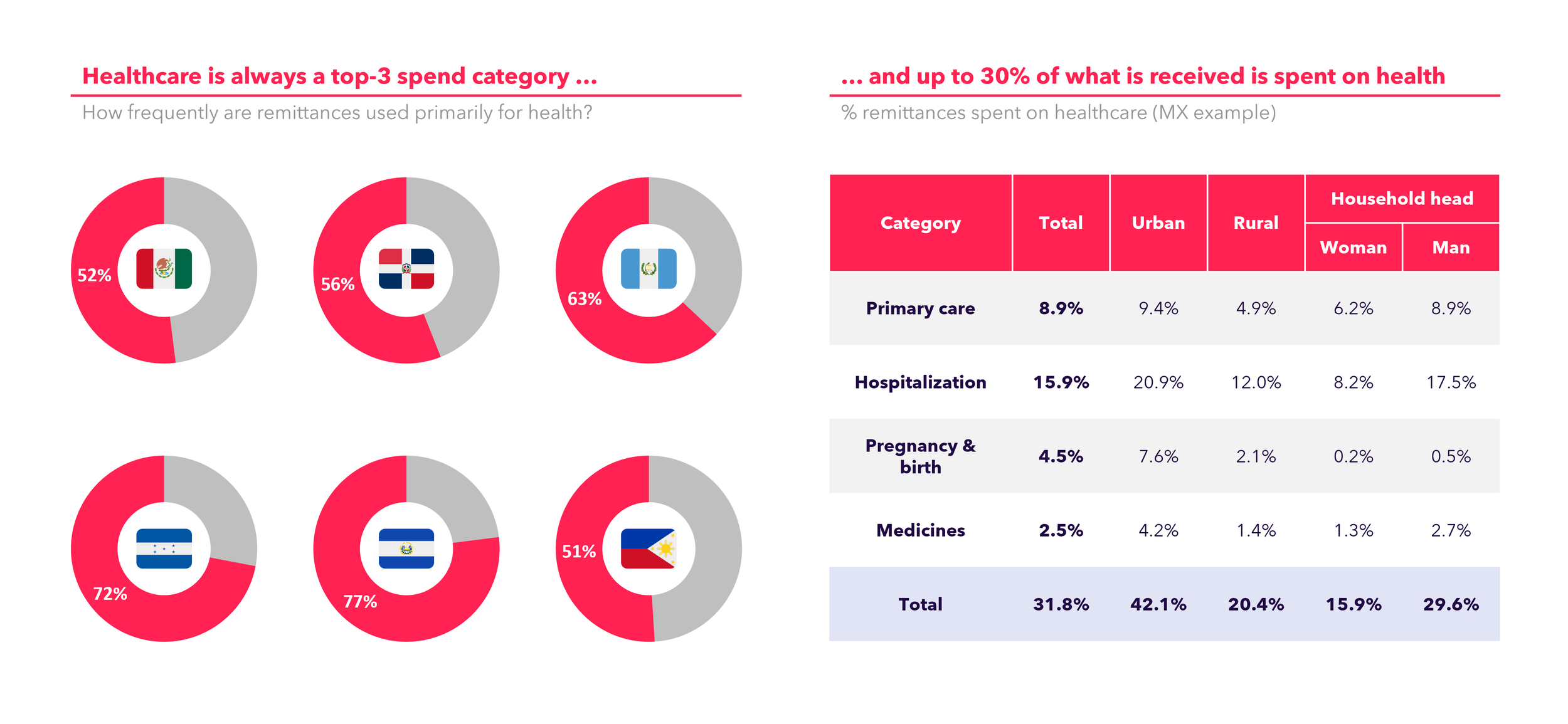

Asistensi launched 3 years ago (March 2020) to both solve the problem and capture the resulting opportunity of offering financial protection in healthcare expenses to the family members of migrants. A massive problem considering that 50 to 80 percent of the USD 750 billion of remittances sent per year are destined partially for the payment of health bills as a primary (top 3) reason and, despite the sheer size of this help, it is not enough because 200 million individuals in countries with high emigration rates fall into poverty every year when a health emergency becomes a financial emergency. To put it simply, the remittances are too little too late and both recipients and senders of remittances could benefit from having financial protection in healthcare expenses (i.e., health insurance) that covers these emergencies.

Source: INEGI, CEMLA

The idea was offering health insurance to migrants to provide health insurance coverage for their families in their home countries. It seems like an obvious business idea, doesn't it? Considering that migrants and the family they support are the third largest economy of the world (check this out). Surely this idea must have been considered before. In fact, we are aware of dozens of projects that attempted to address this previously and never successfully launched or did so in a compliant (hence sustainable or scalable) way. Why is this problem so challenging? There are two major reasons (1) health insurance as we know it does not properly address their problems and (2) regulation makes extremely tricky to sell insurance cross border.

Solving problem #1: A new kind of health insurance

Migrants needed a different approach to health insurance. First, migrants tend to care for people that are traditionally excluded from insurance companies. For example, their grandma, grandpa or mother are older than the typical 65 years old cut-off. Second, they have limited budgets and cannot afford insurance plans that have large limits or cover preventive care. Nevertheless, families of migrants get sick like everyone else so traditional so called ‘micro-insurance’ offerings are actually worthless to them. Finally, they do not have the luxury of being able to pay deductibles or provide financial guarantees (e.g., credit card) at the moment of admission of the hospital. Therefore, conventional health insurance does not work for them.

We needed a product that:

Was affordable. Our research told us that migrants with moderate and moderate-low income would be able to pay in the range between 30 to 60 USD per month for healthcare for their families in their home countries.

Covered the healthcare not only with financial support but also with immediate companionship since the migrant is not in the country to drive grandma to the hospital if she is sick.

Albeit it always sounds great to talk about preventive care, there was no need to cover preventive care such as a yearly checkup because it is a luxury to them (they do not do it anyways) and it dramatically increases the cost of the premium. Also, we could not cover catastrophic events such as kidney failure because they would also make the premium too costly and the public system would take care of it eventually with enough waiting. (check out why these two exclusions are relevant)

Covered people above 65 years old because they need to care for mom, pop, and grandma.

Underwriting was so simple that you could answer the health questions on behalf of your mom with a maximum of five straightforward yes or no answers (e.g., did your mother had cancer) without the need to know her complete medical history.

Had no deductibles or financial guarantees. These customers do not have the ability to provide financial guarantees nor the luxury to pay for deductibles.

Thus, we built a product that had two components:

Coverage for primary outpatient care: It provided unlimited coverage for curative outpatient services, excluding preventive or chronic care. These services included telemedicine, delivery of medicines, visit of a doctor to your home, basic lab tests and ambulance services. These services were in fact built in as a gatekeeper to avoid unnecessary visits to the hospital while at the same time provide the necessary and timely medical care. However, to the eyes of the customer it never felt like a gatekeeper but instead as a benefit of great customer experience because they had immediate and continuous medical support.

Coverage for inpatient hospitalization and surgery: only if the condition could not be treated through outpatient primary care, and with the approval of one of our doctors, we provided coverage for inpatient hospitalization and surgery, specifically for curative purposes (again, not preventive or chronic). The coverage amount ranged from 3,000 to 15,000 USD per event per year, varying based on the country and product. Actuarial reasoning supported that this coverage would address 80% of the most common health emergencies in those countries and in fact it was even better than that because less than 10% of our customers ever had to pay for any portion of a hospital bill.

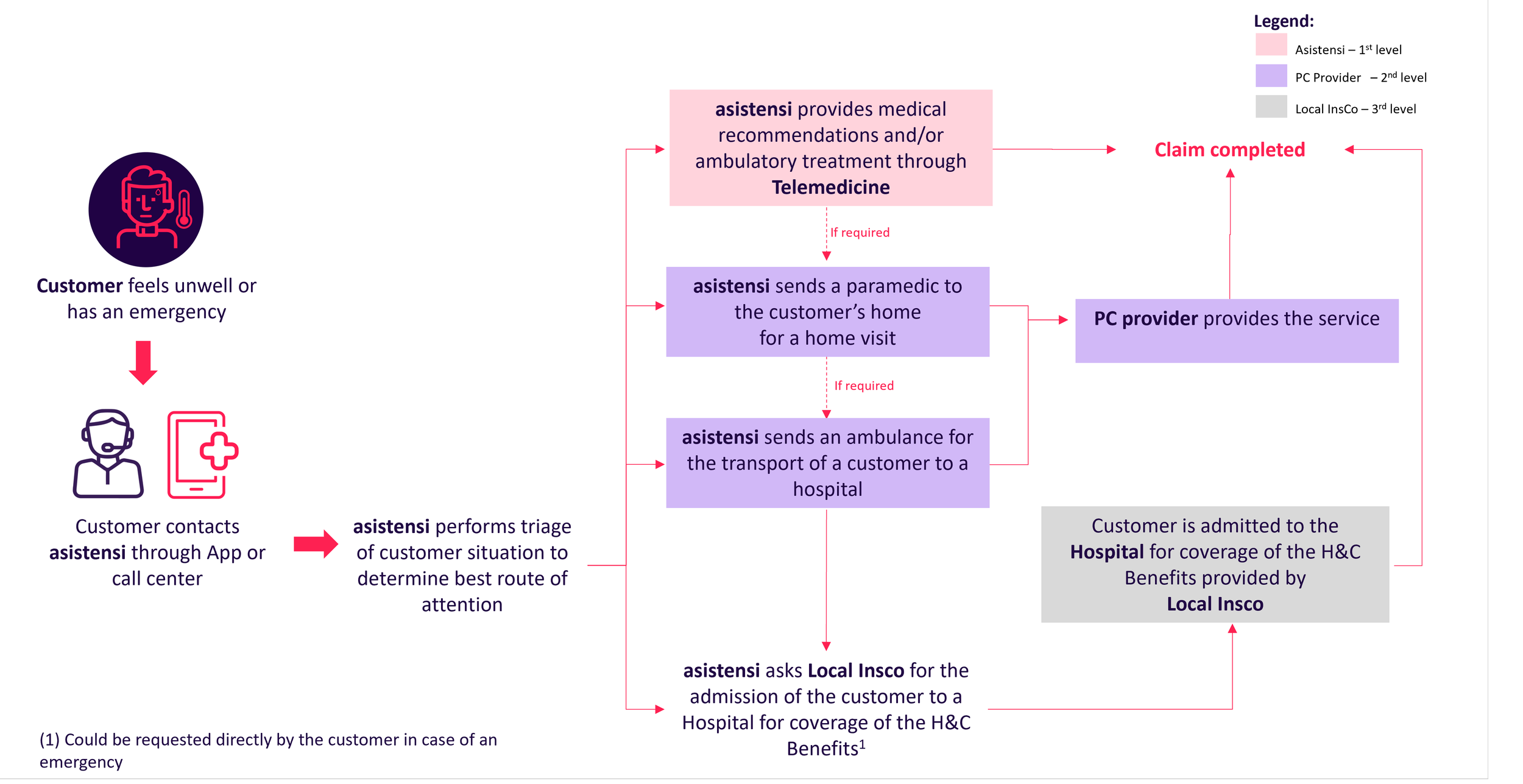

This was the value proposition for the customer for each of our countries - Venezuela / Dominican Republic / Mexico / Philippines / Guatemala / Honduras - and this is how the process worked and it all came together:

Our operating model

The result? excellent customer experience as measured by 4.3 Trustpilot score and 80%+ NPS plus an amazing efficiency as measured by a 50% medical loss ratio. Check out our operating KPIs here.

Our operations relied on an internally built CRM for managing customer claims through the entire process known as the Emergency Management System (EMS) enabling our Doctors to triage, route and follow up on cases (demo video here). This allowed us to handle three to four thousand services per month with a process that had a lot of moving parts (e.g., 55 different providers across 6 countries) where the life of our customers depended on it and every second counted.

And by the way, the price was up to 30% lower than comparable alternatives and we also were able to accept monthly payments in cash at over 18,000 points of sale and accepted most payments methods known to man. With regards to payment frequency, you could have picked monthly, quarterly, biannually and annually which was also a key requirement for a population that - more often than not - goes from month to month.

Price benchmark for most comparable product in Mexico during 2022, Asistensi Light. Dotted line denotes that is not sold for new customers, only for renewals

All of this was conducted on our own proprietary custom built core platform that managed and processed payments, policy renewals, and expirations for more than 12 products with over 1,800 pricing constituents in 6 countries.

Startups typically offer advantages in terms of price or growth through three different approaches. First, burning investor’s money like it’s 2021 – which was not our case. Second, faulty actuarial calculations or negative risk selection in target populations (e.g., going after customers spurned by traditional providers and hence are happy to purchase your product but will yield higher losses) – which was not our case either. Third, doing things differently which was our case with our model. Ultimately, the proof that our model worked and that the price advantage was really sustainable lies in our medical loss ratios and customer acquisition expenses.

Here you can find more detail on the excellent loss ratios and on CAC being below actuarial limits.

Solving problem #2: making regulation work for cross border insurance

Not everyone knows this or needs to know this but unlike banking regulation which aims to prevent bank runs and protecting customer deposits by mandating adequate and sufficient risk management of assets and liabilities, insurance regulation primarily focuses on safeguarding customers from insurance companies failing to fulfill their promises or ensuring the fairness of such promises. To put it bluntly, insurance regulators are like courts of customer complaints. Hence, insurance regulators are unwilling to allow insurance companies from other countries to operate within their jurisdiction due to the lack of authority to enforce regulations against these foreign companies when necessary. Similarly, regulators are hesitant to permit insurance companies based in their country to conduct business in foreign jurisdictions as they do not wish to engage with foreign courts and handle complaints in jurisdictions where their authority does not extend. Therefore, the following applies for all countries:

In the countries where the migrant would be interested in purchasing insurance from, such as in the USA, EU or UAE:

Foreign insurance companies cannot issue policies or solicit customers.

Insurance distribution activities can only be undertaken by a locally authorized and supervised entity.

In the countries where the family member would be covered, which in our case was Mexico, Philippines, Guatemala, Honduras, Dominican Republic and Venezuela:

Residents can only be insured by a local insurance company.

Such policy needs to be directly issued to the policy holder (reinsurance does not work).

Local insurance companies cannot issue policies abroad.

So… how did we solve this and become the first and only company in the world that could sell insurance cross border in a compliant way?

The short version? We issued two policies as follows:

One in the origin market where the migrant was the policyholder and included both the primary care outpatient coverage and the hospitalization and surgery inpatient coverage. The latter was a mirror policy of the destination market coverage. This policy was an individual contract that was issued either by our own insurance carrier in the US or our fronting partner in the EU and then reinsured to our captive carrier.

Another one in the destination market were Asistensi was the policyholder and covered only the hospitalization and surgery inpatient coverage. This policy was a group policy issued by a local carrier (always the #1 ranked player in the country) and the beneficiaries were the family members of the migrants. Primary care outpatient coverage was provided as a service since this is not an insurable risk in most jurisdictions.

We used a captive carrier in an international jurisdiction as a pass-through to be able to “connect” both policies. In our case this was in done in Barbados but could be done elsewhere.

This required a significant regulatory stack of assets and agreements that took blood, toil and sweat to build and is summarized in the chart below. The hardest part was persuading regulators (and notably your friendly compliance officers of partner carriers) in a synchronized manner that this solution not only operated effectively within their respective jurisdictions but also complied with the regulations of other jurisdictions who were in turn doing the same validations in some sort of regulatory catch-22.

A list of all the licenses we obtained to be able to underwrite and enable cross-border insurance

The long version? this document here has a detailed explanation for those with the legal curiosity.

The ride of a lifetime

We launched our product in march 2020 in the market we knew best and could bootstrap assets available to us the most: Venezuela. I am Venezuelan and so were my partners so this was a natural testing ground before going to larger markets. Once we had about 400 live policies and the data to back up that our model and proposition worked we went out to raise capital as to launch in the two most attractive markets for remittances in LATAM: Mexico (USD 54 billion in remittances) and the Dominican Republic (USD 11 billion in remittances). In July we received a term sheet for our seed round from the amazing Javier Santiso and Lluís Viñas (Mundi Ventures) who coincidentally were the first persons I wrote to when I started fundraising since they have the best insurtech fund in Europe. Nazca from Mexico joined as a co-lead whom I also regarded as the best fund in Mexico, a crucial market for our future.

After a year, we launched in the Dominican Republic and were waiting for regulatory approval of our product in Mexico. However, our key performance indicators (KPIs) for loss ratios, customer acquisition cost (CAC), and customer experience were excellent and we were growing 20% month over month. As a result, our existing investors pre-empted our Series A process with a friendly term sheet to quickly open central America and Southeast Asia. For this round, we had Alexander Kudlich from 468 Capital, one of the most prominent figures that has shaped Europe's entrepreneurial ecosystem as we know it, leading the investment. Armed with new funds and a favorable investment climate that supported bold growth, we ventured to open operations in Honduras, Guatemala, and the Philippines. From June 2021 to September 2022, we successfully and quickly expanded into new countries, averaging one new country every three months.

Asistensi Dominican Republic advertisement

Why did we expand so rapidly into so many countries? Basically, because we wanted to build an unfair competitive advantage in our go-to-market. That is, we believed that synergies in customer acquisition and costs of our regulatory stack existed in the markets were migrants lived if you could address more markets where migrants come from. In other words, by targeting multiple nationalities simultaneously, we could unlock larger synergies and create a bigger competitive moat. Moreover, the expenses associated with entering and operating in a new country were relatively low, as the majority of costs were concentrated in our origin markets (US, EU). In hindsight, it's easy to see that perhaps we should have focused on fewer markets if we had known that the investment sentiment was going to turn south and quickly. However, at that time, based on the available information and the investment market of the time, we made the decision to pursue multiple markets.

During our peak, we had over 260 employees. One of the most important reasons for me to go out and build Asistensi was (i) to create a place where people would not say hi to each other in the elevator on Mondays with phrases like “good morning and pretend it’s not Monday” and (ii) create a platform where exceptional people would grow and everybody had a meaningful career path. While we may have made some mistakes along the way, I firmly believe that we successfully defined the right target culture (summarized in our values, code of ethics and performance management framework) that would have fulfilled this purpose and that we were progressing firmly in their adoption. One thing that gives me immense pride about Asistensi is the incredible team we assembled. To all of them, I extend my heartfelt gratitude for everything you did. Here are just a few examples of the exceptional individuals who contributed to our success: find their names here. Thank you!

We were actively working on transforming the health and insurance systems to ensure inclusivity and accessibility for those who needed them the most. One crucial aspect that demanded a radical transformation was the approach to insurance promotion. This is because:

We firmly believed that establishing a direct relationship with our customers, rather than relying on brokers, was crucial for delivering a more efficient service. This approach was particularly vital in our model, where our physicians provide continuous support to customers from initial orientation to clinic discharge. Additionally, our exceptional team of commercial advisors is adept and trained at explaining the benefits and limitations of our product with complete transparency, surpassing the doings of any broker.

We strongly believed that migrant communities and individuals excluded from health systems should be the primary beneficiaries of the economic opportunities presented by promoting products and services like ours. Through Asistensi, we aimed to become not just a company that provides protection for family members but also a source of economic empowerment, ensuring these communities have the means to put food on their tables.

We wanted to build on the tremendous value of trust conveyed by these communities and the power of a positive recommendation. While our customers seldom placed trust in institutions like banks or insurance companies, they relied on the trust within their communities or the recommendations of acquaintances. Thus, earning the trust of community affiliates plays a pivotal role in gaining the trust of our customers. We firmly believed this should be our primary customer acquisition channel.

To address this, we developed an MLM affiliate program with a crucial distinction: its primary focus was to generate customer leads rather than selling insurance directly. Customers belonged to us, and affiliates were not involved in the sales or claims process. At its peak, the program boasted 2,500 affiliates spread across 115 cities, achieving an impressive lead to conversion ratio of 40%. Notably, it played a significant role, contributing to nearly 50% of our overall sales. To support our affiliates, we developed an exclusive platform that enabled them to track their income, generate leads in full compliance, manage their network of promoters, and access various tools including customized hyperlinks, training materials, and social media content. (You can check out the summary of the proposition here)

When time ran out in May 2023, we had over 40,000 members spanning across 55 countries, providing coverage through over 12,000 live policies in 6 countries, we were generating more than USD 600,000 per month in GWP and were ensuring a seamless delivery of a health service every 10 minutes, catering to individuals in 14 different time zones.

At the end, these are just numbers, what really mattered was the impact we had on so many people’s lives like Carmen below.

The story of Carmen

How did it end and why did we fail?

We failed mainly because we ran out of time in the middle of an unprecedented venture capital market meltdown. Fundraising winds changed drastically when our sails were fully deployed towards market expansion and our burn rate was too high and our runway too short.

We tried raising a Series B round and even managed to secure a binding term sheet from a strategic lead investor in November 2022. It was a USD 17mm round that unfortunately fell apart after three months of closing work and left us with one month of cash in the bank. (why they pulled out? mainly due the fact that key elements of the agreement such as an equity kicker and a warrant could not be implemented under Spanish law without implying realized tax liabilities for unrealized gains. This is one of several problems that the spanish legal system poses to entrepreneurs hence I would suggest others to establish their holding companies elsewhere ).

However, in hindsight, there were a few areas where we could have performed better besides expanding too quickly that would have helped with fundraising and perhaps would have given us more than one term sheet as to avoid the fallout when the strategic investor pulled out, most notably:

We did too little too late to control customer churn in our second largest market (although elsewhere it was not a problem this was a bad omen for some investors).

We invested too much of the development bandwidth for our tech platform into launching new markets and postponed too much the creation of efficient processes which in turn snowballed manual processes, headcount and ultimately burn.

In some markets our local insurance partners gave us prices that did not fully reflect the risk reduction of our model and were enjoying loss ratios in the 30 to 40 percent range. We took the decision to launch with smaller margins in a “build it and they will come” mentality counting on our ability to negotiate better prices along the way. This proved to take more time than expected and the necessary prices from our partners to have the required margins did not materialise until it was too late.

We had a global-local governance model where functions like growth were global in the Madrid HQ in order to benefit from scale and specialisation but responsibility of meeting sales targets was in the countries. This not only generated a lot of friction between teams when accountability overlapped (e.g., are the leads not converting due to sales team practices or due to lead quality?) but also I wonder if it had been better to have the HQ in a large country like Mexico instead of Madrid to make sure we could win that market quickly.

Also, unfortunately we launched and achieved scale in a market that was untouchable to many investors (or seen as an outlier given it’s mind-boggling dynamics) – Venezuela- despite this actually reflecting our execution capabilities in extremely difficult markets.

To my team I remind them that we failed while “daring greatly, so our place will never be the same of those cold and timid souls who neither know victory nor defeat” (Roosevelt). Moving forward I hope and encourage that you “stay wild and young, may your limits be unknown and your efforts be your own” (The Killers). I am incredibly grateful to have embarked on this journey with you and to collaborated with a group of talented and motivated individuals like yourselves. We built boldly and now is time to fail while proudly looking forward.

What happens now with Asistensi?

The company has been taken over by bondholders (Grupo Venemergencia) with the intention to carve out and liquidate it to partially recover their losses. We reached this point after they lent us a few months of runway when the Series B round fell apart as we scrambled to find additional funding but weren’t able to do so. They plan to continue operations in Venezuela and potentially the Dominican Republic, but only for local customers and without the international insurance aspect. Customers in the rest of countries will be adequately serviced until their insurance contracts expire. Notably, they will sell our valuable regulatory stack to an American TPA (still subject to regulatory approvals) as to recover some their losses and make sure that the licenses remain well capitalised. In any case, customers, employees, and affiliates in Venezuela and the Dominican Republic can rest assured in the fact that the business will continue strongly there with the adequate financial support, although it will likely operate under a different brand name.

The occasion to create anew again

Sometimes, despite giving it your all, things just don't work out. Asistensi was a remarkable project that had a positive impact on many lives and held immense potential. It was created with intention, creativity, purpose, care, and the expertise of numerous individuals.

However, fate, as it has done with countless other extraordinary ventures, decided that it had to come to an early end.

I consider myself a builder and a fighter, always ready to rise again and embark on new ventures. A setback merely sets the stage for an incredible comeback.

I would like to thank our investors once more for all the support and conviction they poured into this project. The road to success is paved with failures, but it is also illuminated by the unwavering support of those who believe in you. Our investors were this light for us all along the way and hope we can repay their investment somehow.

One positive aspect of concluding a project like this is the boundless opportunities that await. I'm currently contemplating what my next great endeavour will be. If you have an idea and are one of the bold and unconventional thinkers, you know where to find me.

Madrid, May 30th 2023

Follow my updates:

I write about two things:

Updates on my current endeavor: the journey of Fintonic.

Buzzworthy facts and insights about the Spanish consumers, distilled from data that is only accessible through the aggregation capabilities of Fintonic. (we have the biggest aggregation data of bank accounts in the Spanish market). Are consumers spending more on Zara or Shein? Is the Spanish consumer confidence high? Find out in my updates.